Today’s Topic: Student Loan Debt Relief Scams, Bankruptcy, Student Loan Forgiveness Numbers, Exposing Scam Companies and Social Media Giants That Aid Them!

Almost every day I receive calls from student loan companies offering me immediate debt relief, loan forgiveness and interventions that will force loan servicers to reduce my debt. Sounds great right? Wrong! These companies are scammers who lure struggling borrowers with promises that are outright lies. Is Your Company On Nerd Wallet’s Watch List? Be sure to check the link below to see if your student loan company is scamming you!

- Tip #1 – How to Quickly Identify Student Loan Scams

- Charge upfront fees

- Promise to have your loans eliminated

- Promise immediate loan forgiveness

- Pressure you to sign up

- Ask you sign a power of attorney to make decisions for you

- You are asked to share sensitive, personal information

- Portray themselves as the Department of Education

- The company advertises on social media or pops up in search engine ads

- Tip #2 – Do you know that not even Bankruptcy will cancel student loan debt!

Unlike other consumer debt such as credit card and mortgage debt, student loans traditionally cannot be discharged in bankruptcy. The occasional exception is the Brunner Test regarding financial hardship.

According to Forbes 2019, “Student loan debt is now the second highest consumer debt category – behind only mortgage debt – and higher than both credit cards and auto loans.” Take a look at Forbes’ statistics:

- Total U.S. Borrowers With Student Loan Debt: 44.7 million

- Student Loan Delinquency Or Default Rate: 11.4% (90+ days delinquent)

- Direct Loans – Cumulative in Default (360+ days delinquent):$101.4 billion (5.1 million borrowers)

- Direct Loan In Forbearance: $111.1 billion (2.6 million borrowers)

- Public Service Loan Forgiveness Statistics

- Number of applications approved: 423

- Number of applications denied: 32,409

- Borrowers who have received student loan forgiveness: 206

Two things pop out when I review the statistics–the default rate and the measly number of individuals who actually received student loan forgiveness!

- Tip #3 – Student Loan Scamming Companies

Now the information you’ve been waiting for regarding student loan scammers. Thanks to the reporting done by Nerd Wallet, you can access a list of student loan debt companies who are scamming borrowers. In fact, former student loan servicer now whistleblower, Bob Greenberg exposes some of the tactics he learned as a manager at Consumer Assistance Project LLC in Coral Gables, Florida. He was trained to tell borrowers anything to keep them on board. Why? Because he earned commissions for everyone he signed up and told them whatever they wanted to hear. He also told borrowers to pay them versus their federal loans and members paid up to $303 per month to Consumer Assistance. The company’s social media ads boasted “Over 5 Million Students Already Forgiven. You’re Next!” and more Facebook ads like “Get Rid Of Your Student Loans Once And For All!” One interesting note is that many of the workers at Consumer Assistance also worked for law firms.

He knew something wasn’t right when each day, Greenberg says, managers gave call-center workers a new, untraceable 800 number for prospective customers to call.

Meanwhile companies like Consumer Assistance Project LLC and others promising debt relief to financially distressed student loan borrowers are siphoning millions of dollars from them with fees for services that never materialize. The student loan industy is ripe for scammers as loans soar to nearly $1.4 trillion according to a NerdWallet investigation. This scam reminds me of the foreclosure defense cases that exploded a few years ago with similar claims.

What is worse for borrowers is to realize that they could have helped themselves for “free” online versus paying a phony debt relief company. To add insult to injury, the borrower believes they are receiving help when what they’ve really done is give permission to the company to scam them. These companies change the borrower’s passwords and then let the account lapse while continuing to auto debit the borrower each month. Then Uncle Sam steps in and begins to garnish wages, seize tax refunds and ruin people’s lives and credit. One woman I met said that Uncle Sam had seized the family home after her mother (borrower) died. Yes, Uncle Sam put liens on the family home then forced the sale to collect on the liens. The daughter is still homeless today. How many other students and their families will end up homeless before something changes?

Thankfully NerdWallet is warning consumers by creating a Student Loan Watch List which has flagged more than 130 businesses who were investigated, sued or penalized and so much more. When you consider Consumer Assistance Project LLC had more than 400 customers who were charged at least $250 a month with gross revenues of about $1.2 million a year, you begin to understand why scammers have chosen the student loan industry. Check out Nerd Wallet’s Watch List here.

Tip #4 – Social Media Companies Let The Scam Continue: The U.S. Consumer Financial Protection Bureau is trying to get big online companies like Google, Facebook, Yahoo and Bing to block advertising by these scam student debt relief companies. Two years after letters were sent to Google, Facebook, Yahoo and Bing, the ads are still allowed to be displayed. What’s interesting is that predatory lenders a/k/a payday loans are being blocked more than student loan scam ads which are much more egregious in my opinion, especially when restitution reveals just how large fraud is in this industry.

Social media responses, “Yahoo had no details on steps taken to block such ads. A spokesman for Microsoft, Bing’s owner, declined to comment. Google and Facebook did not respond to interview requests” according to NerdWallet.

Step #4 – Let Your Voice Be Heard! Tell Google, Facebook, Microsoft and Bing that by not blocking these ads they are colluding with these scam artists in committing crimes against student loan borrowers and their families. It must be stopped!

Don’t forget to call/write Congress and tell them to “wake up” and start working on a solution to the problem before it spirals out of control! Can you imagine if everyone defaulted? What a mess that would be. As I have said before, “capitalization” of interest is the primary reason why student loan debt is spiraling out of control thereby causing more students to default!

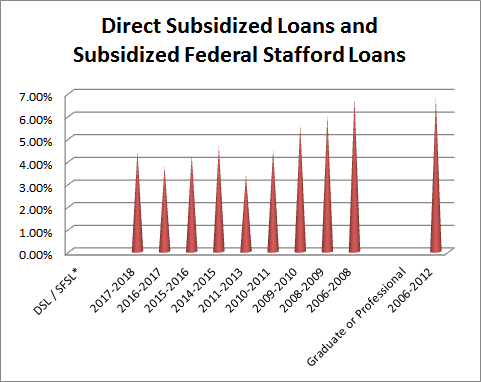

*Picture courtesy of Frumforum.com